Climate risk is already embedded in investor portfolios but it does not always show up in prices. Our research shows that climate risk is only priced under certain conditions, with important implications for bond markets, inflation, and portfolio strategy.

Climate risk affects financial markets and asset prices, but not in a consistent way. The key question is not whether it matters, but when it matters, and how it transmits across asset classes. For investors, this distinction is critical as climate risk is not priced uniformly; its impact is conditional, uneven, and shaped by broader market conditions. Our findings show that climate risk does not operate as a constant market force, rather its effects strengthen in some market environments and weaken in others, with important implications for bond markets and inflation expectations.

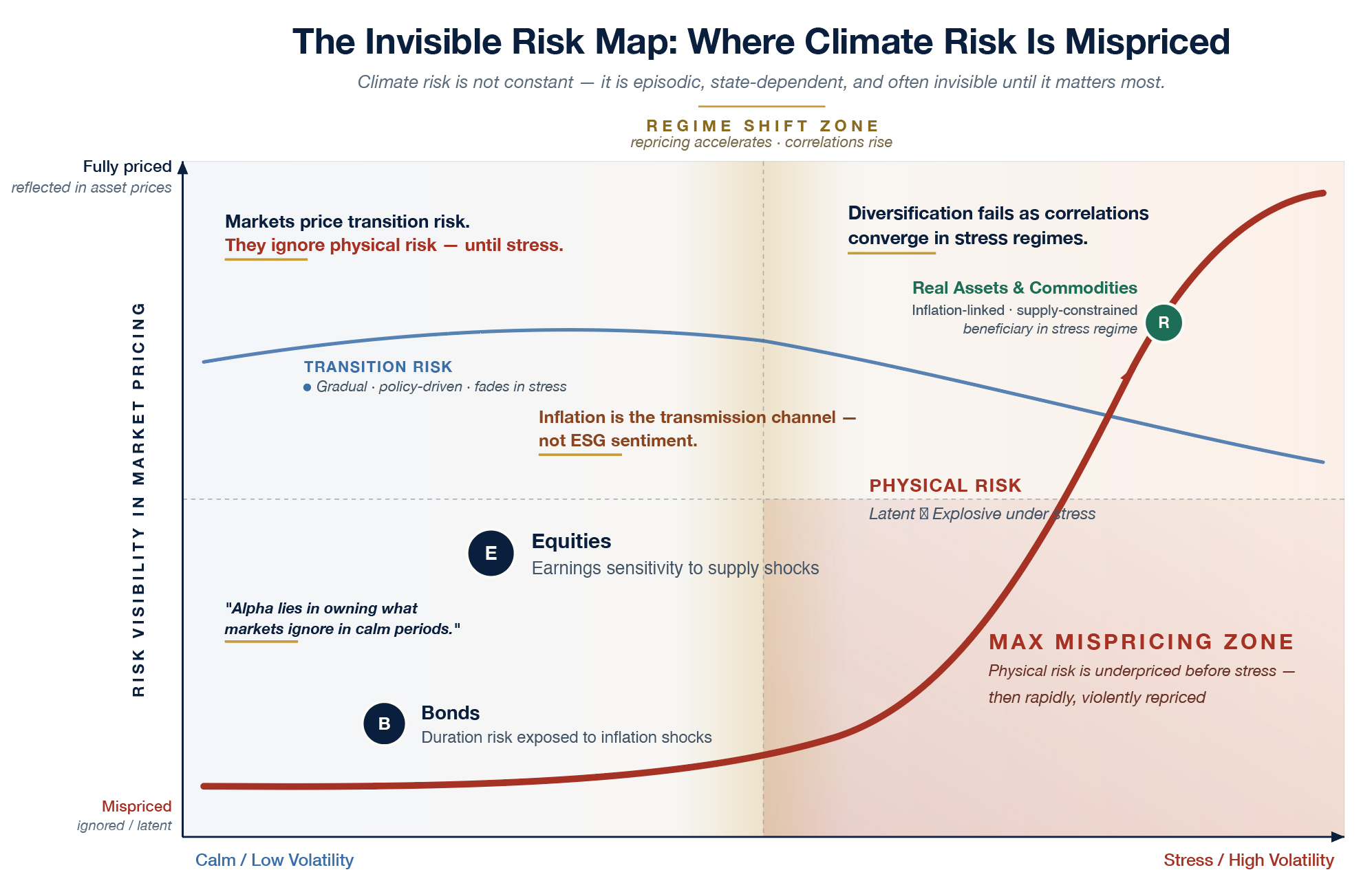

Climate Risk Is Not a Single Risk

Climate risk is not one-dimensional. It operates through two distinct channels:

- Transition risk: driven by policy changes, regulation, carbon pricing, and technological shifts

- Physical risk: arising from climate events such as heatwaves, floods, and supply disruptions

These risks differ not only in origin, but in how markets respond to them. Our analysis shows that transition risk has limited, and at times slightly disinflationary, effects primarily during stable market conditions. In contrast, physical risk is far more disruptive, pushing up short-term inflation expectations and depressing bond returns, particularly during periods of financial stress. This asymmetry is important because it suggests that markets are not simply pricing climate risk as a single concept. Instead, they respond differently to distinct types of climate shocks, with materially different financial consequences.

A Critical but Often Overlooked Dimension: Market Regimes

The most important insight from our research is that climate risk pricing is state-dependent, in that it changes depending on the broader financial environment. For investors, central banks, and market participants, this is a critical point: climate risk does not behave consistently across market conditions. We identify two distinct regimes:

- Low-volatility regimes, characterised by relative stability and persistent market conditions

- High-volatility regimes, associated with financial stress, uncertainty, and shorter-lived market episodes

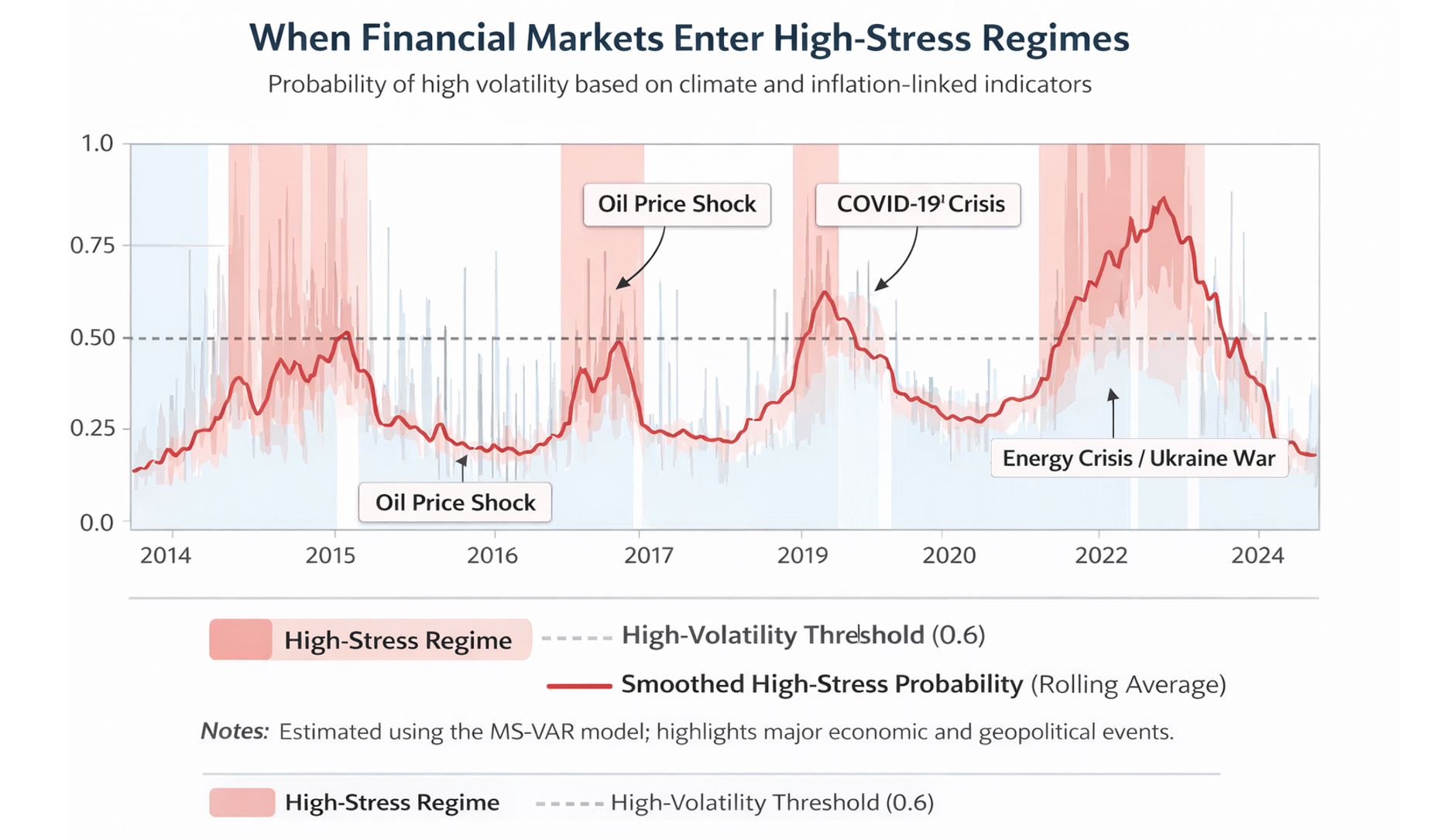

The figure below illustrates how the probability of high-volatility regimes evolves over time, highlighting periods when financial markets transition from stable conditions to episodes of stress.

Rather than focusing on short-term fluctuations, the smoothed line captures broader shifts in market conditions. Periods shaded in red indicate sustained episodes of elevated volatility, where financial stress is more likely to influence asset pricing dynamics. Several key patterns emerge. First, high-stress regimes are not constant but occur in distinct clusters, often aligned with major macroeconomic and geopolitical events. Episodes such as the oil price shock, the COVID-19 crisis, and the recent energy crisis are clearly visible as periods where the probability of financial stress rises sharply. Second, these regimes are relatively short-lived but highly impactful. While calm periods tend to persist, stress episodes are more abrupt and coincide with heightened uncertainty and stronger cross-market linkages.

The behaviour of climate risk across these regimes is fundamentally different. In stable environments, markets tend to absorb climate-related information gradually. By contrast, during periods of stress, risk transmission intensifies, linkages across asset classes strengthen, and shocks propagate more quickly through the financial system. In other words, climate risk is not just priced differently across market conditions, it is amplified when volatility is high.

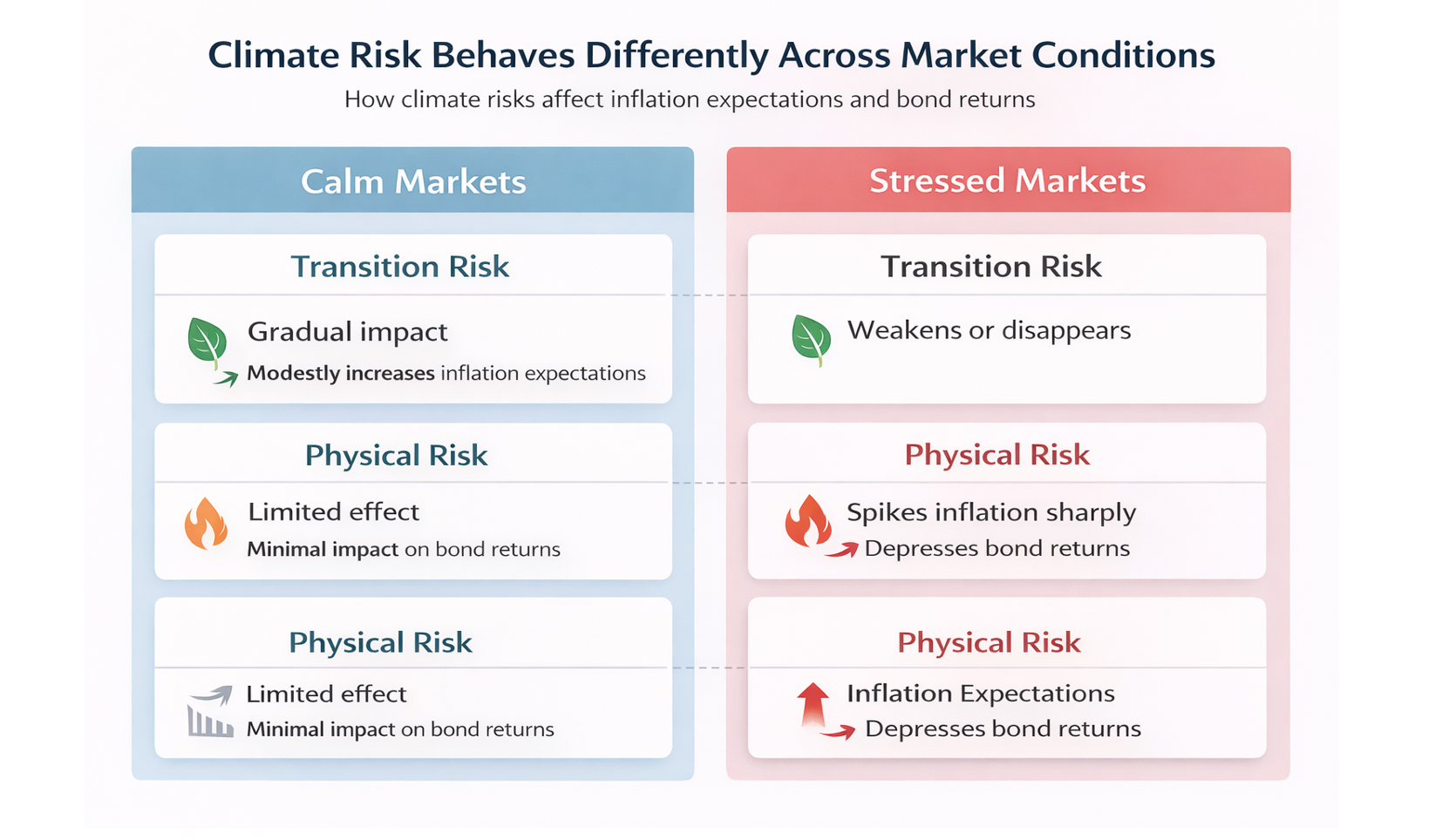

This difference in behaviour across market conditions is illustrated in the figure below which summarises how transition and physical climate risks affect inflation expectations and bond markets under calm and stressed environments from our findings.

In Calm Markets

In low-volatility regimes, markets behave in a relatively stable and predictable manner, with limited cross-asset spillovers.

- Transition risk is incorporated, but only modestly, with effects concentrated in short-term inflation expectations

- Bond markets show limited responsiveness, with sovereign and corporate bonds largely unaffected by shocks

- Inflation expectations adjust primarily at the short end, while long-term expectations remain anchored

In these conditions, financial markets act as relatively effective processors of climate-related information. However, this adjustment is muted rather than strong which is consistent with our finding that transition risk has a limited and mildly disinflationary effect, and only in stable market environments

In Stressed Markets

This dynamic changes significantly in periods of financial stress.

- Transition risk effects weaken or disappear, becoming largely insignificant

- Physical risk becomes the dominant driver, exerting a destabilising and inflationary impact

- Bond market linkages strengthen, with clear evidence of contagion and amplified spillovers across asset classes

- Short-term inflation expectations react strongly, while long-term expectations remain comparatively anchored

During these periods, markets shift their focus toward immediate and material risks, such as energy price shocks, geopolitical disruptions, and broader macro-financial instability. As a result, longer-term transition dynamics are effectively crowded out, while physical climate risks are rapidly transmitted through the financial system. This is reflected in stronger comovement across assets and heightened sensitivity to shocks in the high-volatility regime

Why This Matters

This leads to a striking but important conclusion: climate risk is not absent from financial markets, it is state-dependent and therefore not always visible in prices. In stable conditions, transition risks are gradually incorporated, albeit modestly. However, during periods of stress, market attention shifts decisively toward immediate physical and macro-financial risks, reducing the visibility of longer-term transition dynamics.

For practitioners, this has several important implications:

- Climate risk may be mispriced during periods of stress, not because it disappears, but because physical risks dominate and distort pricing dynamics

- Market signals are regime-dependent, and therefore cannot be consistently relied upon for forward-looking climate risk assessment

- Risk management frameworks must account for non-linear dynamics, including contagion effects and amplified spillovers in high-volatility environments

- Policy interventions may need to address these regime-specific blind spots, particularly where market-based signals underrepresent longer-term transition risks

Overall, the findings highlight that climate-related financial risk is not only a question of magnitude, but of timing and market conditions with important consequences for asset pricing, portfolio allocation, and monetary policy design.

Inflation Expectations: The Core Transmission Channel

A central finding of our research is that climate risk affects financial markets primarily through inflation expectations, rather than through direct asset pricing effects alone. However, this transmission mechanism is strongly horizon-dependent.

- Short-term inflation expectations react significantly to climate shocks

- Long-term inflation expectations remain largely anchored

This divergence reflects two distinct underlying dynamics:

First, short-term expectations are highly sensitive to supply-side disruptions.

Physical climate shocks, such as extreme weather events, disrupt production, energy supply, and logistics chains, generating immediate upward pressure on prices. Second, long-term expectations remain anchored by central bank credibility.

Markets continue to price in a return to inflation targets over time, reflecting confidence in monetary policy frameworks. This suggests that climate risk is currently interpreted as a series of transitory shocks, rather than a persistent structural driver of inflation.

However, this perception may shift as climate shocks increase in both frequency and severity.

Bond Markets Under Climate Stress

The implications for bond markets are both subtle and regime-dependent.

Physical Risk: A Destabilising Force

In periods of heightened volatility, physical climate risk acts as a system-wide shock:

- Depresses returns across both corporate and green bonds

- Pushes up inflation expectations

- Strengthens co-movement across bond classes

These effects reflect a combination of:

- Rising expected costs for firms

- Increased uncertainty around economic growth

- Higher risk premia demanded by investors

Overall, physical risk behaves as a macro-financial stress amplifier, rather than a sector-specific shock.

Transition Risk: Conditional and Secondary

By contrast, transition risk plays a more muted and context-dependent role:

- Its effects are modest in magnitude

- It is primarily priced during low-volatility periods

- Its influence diminishes during episodes of market stress

This does not imply that transition risk is unimportant. Rather, it may be overshadowed by immediate macro-financial concerns during crisis periods.

Green vs Conventional Bonds: Limited Differentiation

A particularly notable result is the lack of strong divergence between green and conventional bonds. Despite expectations that green assets might offer greater resilience:

- Their return dynamics closely mirror those of conventional bonds

- Differences are limited, especially during periods of stress

This suggests that market-wide factors, such as liquidity conditions, risk sentiment, and macroeconomic uncertainty, currently dominate sustainability characteristics in driving bond performance.

When Diversification Breaks Down

An important implication of the results concerns the state-dependent nature of diversification. Under normal market conditions, bond segments retain some degree of differentiation, allowing diversification strategies to function as expected. However, this changes markedly during periods of stress:

- Correlations across bond classes increase

- Contagion effects intensify

- Asset returns become more synchronised

As a result, climate-related shocks reduce diversification benefits precisely when they are most needed. This reflects the broader finding in the paper that physical risk operates as a system-wide shock, compressing cross-asset dispersion.

A Subtle but Important Policy Insight

The findings also reveal a timing asymmetry in how markets respond to climate policy signals. In stable market environments:

- Transition risks are actively processed and priced

- Policy signals can meaningfully influence capital allocation

In contrast, during periods of market stress:

- Investor attention shifts toward immediate macro-financial risks

- Climate-related signals lose impact

This suggests that the effectiveness of climate policy is conditional on financial stability. Delaying policy action until crisis periods may therefore limit its ability to shape market behaviour.

Implications for Investors

For institutional investors, including asset managers and long-term capital allocators, the results point to several key insights:

1. Climate Risk is Regime-Dependent

Climate risk does not operate as a constant pricing factor. Its impact varies with:

- Market volatility

- Macroeconomic conditions

- Investor attention

2. Physical Risk Dominates in Stress Periods

While transition risk is central in policy debates, the paper shows that physical risk drives market outcomes during high-volatility regimes. This has direct implications for:

- Stress testing frameworks

- Scenario design

- Portfolio risk management

3. Inflation Expectations as the Transmission Channel

Consistent with the paper’s core contribution, inflation expectations are the primary channel through which climate risk affects financial markets. This links climate shocks directly to:

- Short-term inflation dynamics

- Monetary policy expectations

- Discount rate adjustments

4. Rethinking Diversification Assumptions

Traditional diversification strategies may be less robust under climate stress:

- Cross-asset correlations rise

- Contagion effects strengthen

- Safe-haven characteristics weaken

This reinforces the need for climate-aware portfolio construction.

From Peripheral to Systemic Risk

While our research finds that climate shocks remain relatively contained within European bond markets, this likely reflects:

- The scale and resilience of the European economy

- Strong institutional and policy frameworks

- Credible monetary policy anchoring expectations

However, the evidence also points to a gradual shift. Climate risk is becoming:

- More frequent

- More tightly linked to macroeconomic conditions

- Increasingly systemic in nature

As this transition progresses, the regime-dependent effects identified in our research are likely to intensify.

Final Insight

The key contribution of this research is not simply that climate risk is priced in financial markets, but that its effects vary fundamentally across market conditions.

- In calm periods, it is selectively priced

- In stressed periods, it is amplified and transmitted system-wide

- At times, it may be temporarily overshadowed by broader macro shocks

Understanding this conditional behaviour is critical because future climate shocks will not only test environmental systems but also the resilience of financial markets themselves.